JHM - April 13, 2024

JHM - April 13, 2024

I am looking after a friend’s dog this weekend. His name is Theo, he is an Australian shepherd, and is a really great dog. Similar in temperament to my late Labrador Murph, Theo also appears very bribable with food. I can personally relate, but that is a different story. The consequence of this is that, similar to how Murph was, Theo is built a little bit like a member of the front row (in rugby speak) or an offensive lineman. Essentially, some junk in the trunk. In much the same way that the U.S. economy is struggling to shed, Theo still carries signs of post pandemic excess, but unlike the participants in the U.S. economy, it looks good and he is happy.

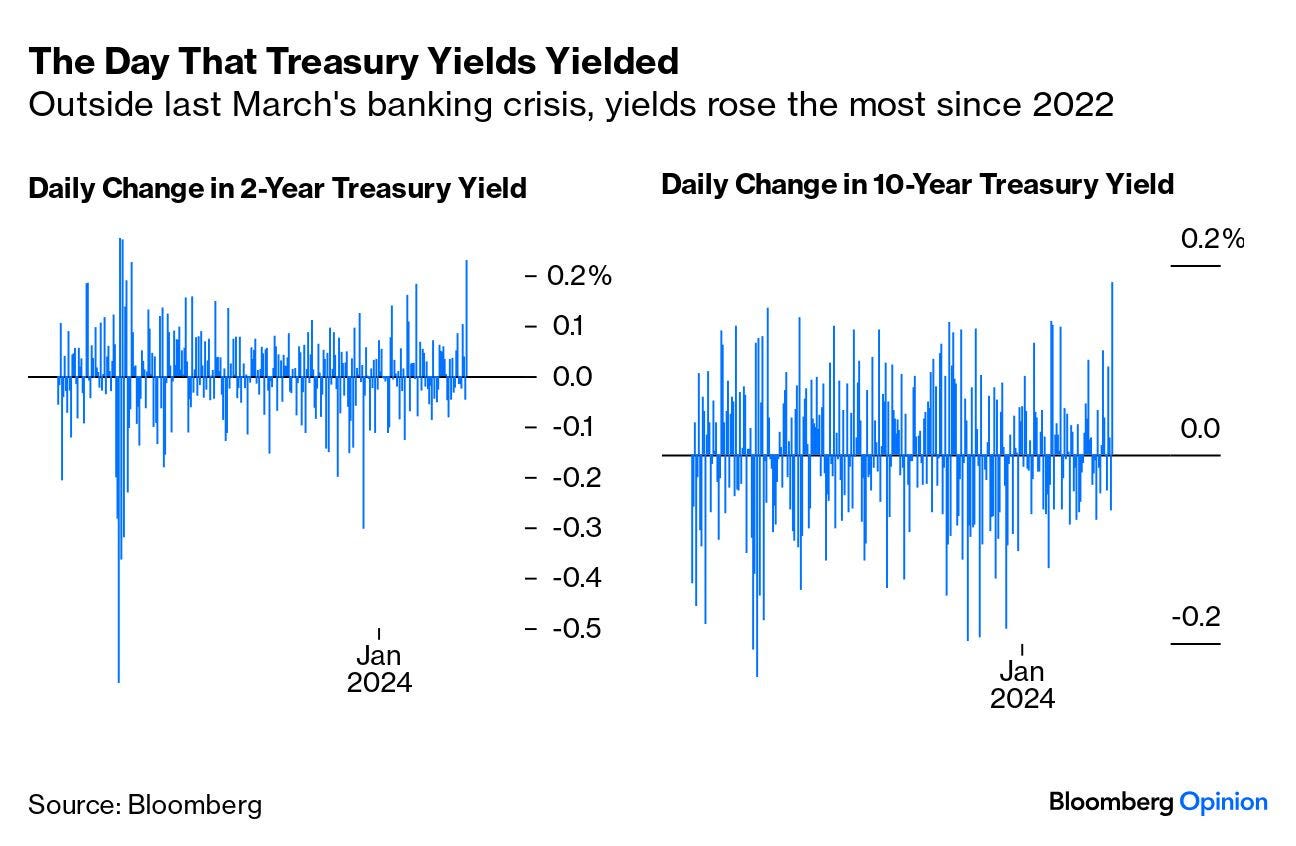

The persistence in elevated inflation readings is problematic for President Biden’s re-election chances, and Powell’s legacy as a central banker. Not to mention the populace that is frustrated with consistently being forced to pay higher prices. It also continues to frustrate market participants desperate for interest rate cuts from the Federal Reserve, and this week’s inflation print added further fuel to the debate as to whether the discussion should really be about the need for hikes and not cuts. We finally got a little bit of excitement Wednesday with the release, which was followed Thursday by the European Central Bank announcement where some dissenters called for immediate interest rate cuts. This kind of divergence between central bank expectations has important implications primarily for the FX market, as was on display with the weakness in the Euro and important technical breakdown.

A stronger USD combined with higher commodity prices is particularly problematic for those countries and parts of the world that are net importers of these increasingly expensive commodities. If the dollar appreciates and the commodity price stays the same, by virtue of the fact that commodities are all priced in U.S. dollars, you can now purchase less than you could before for the same amount. Similarly, if the price of the commodity goes up but your currency is unchanged. Add the two together and you get a significant squeeze on the purchasing power of commodity importers. A case in point would have been Europe in 2022 when gas prices surged alongside the collapse in the Euro, putting pressure on the economy.

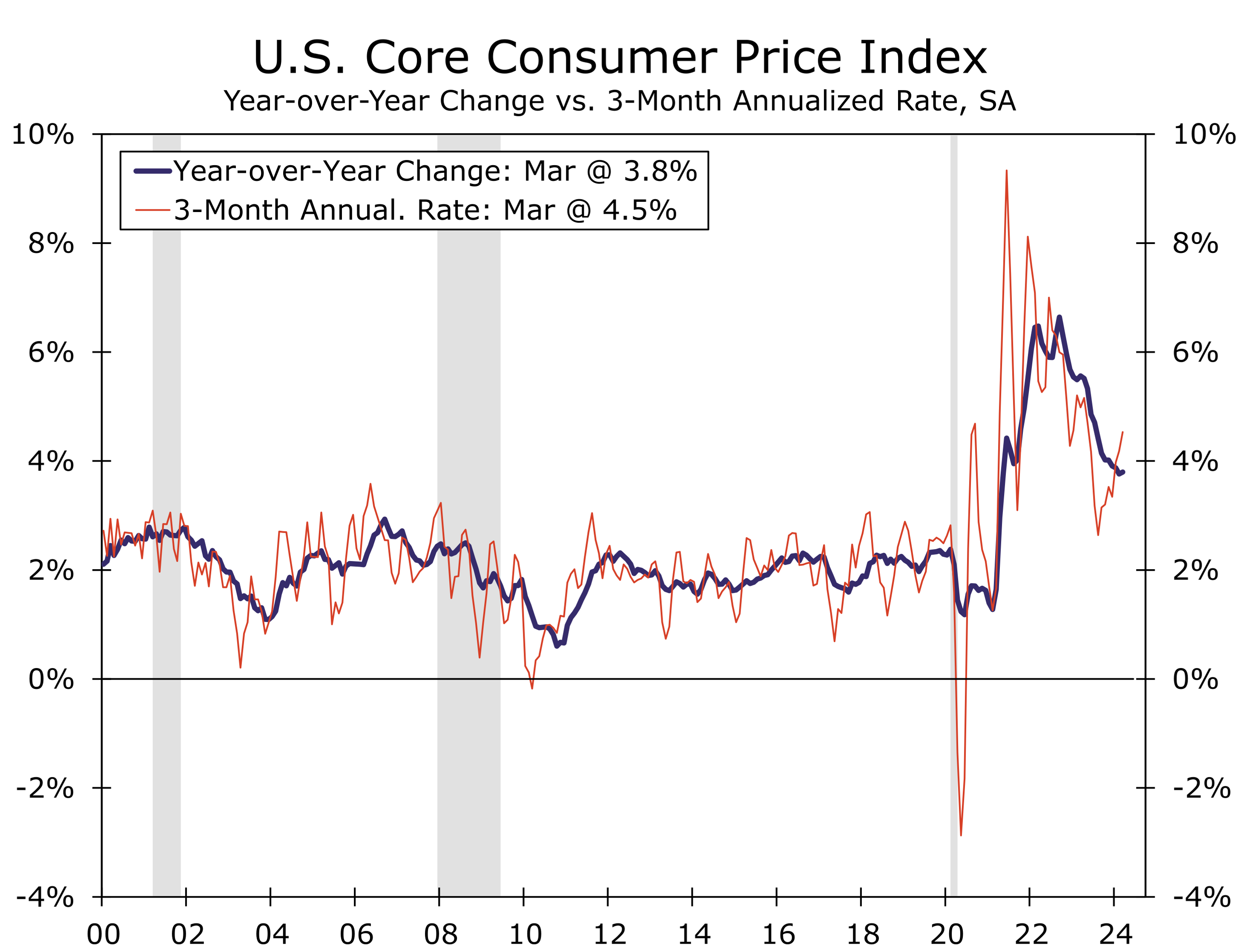

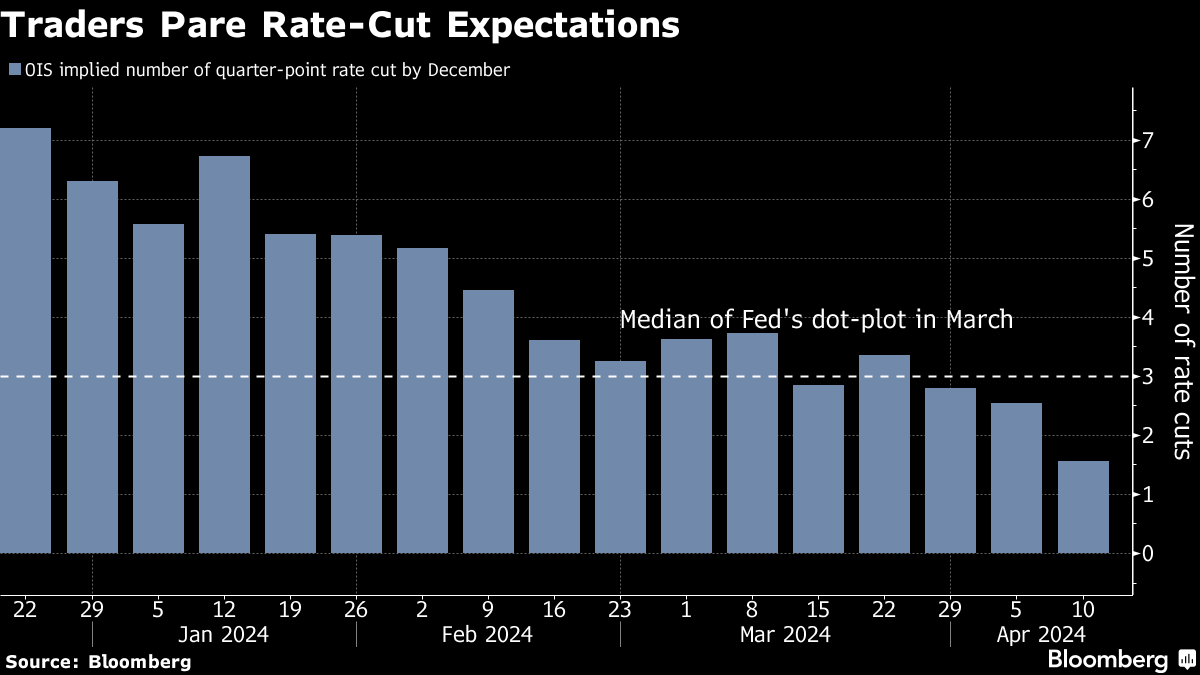

The print this week showed the third consecutive month of U.S. inflation at +0.4% month-on-month, putting the year-on-year rate at 3.8%, well in excess of the Fed’s 2% target for price stability. The reality is that with the government’s debt load as high as it is, they need some inflation to bring down the real interest rate (nominal minus inflation) on the debt outstanding. The issue is that these elevated inflation readings are causing significant re-pricings of expectations for future cuts/hikes, pushing borrowing costs higher at every tenor for the Treasury. Having started the year with almost 100% certainty the first rate cut would arrive in March, we are now down to approximately just a 20% likelihood of a cut in June.

What is driving the persistence in inflation? There were plenty of areas where prices were actually lower than the previous month, most notably airfares, new motor vehicles, and recreation services. However, these were offset by elevated motor insurance and repair costs – you can buy the car cheaper; it is just now significantly more expensive to keep it. Shelter costs continue to confuse, as the expectation was the elevated readings of recent months would have dissipated by now as more “real-time” indicators of housing and rental costs have been coming lower, and yet there remains some disconnect.

Conversely, the ECB looks set to cut rates in June. The inflation shock in Europe was primarily driven by the surge in energy prices following the onset of the war in Ukraine. Since energy prices are significantly off their highs, inflation is at a more manageable level that gives Christine Largarde the confidence to embark on the cutting cycle. As she noted in the press conference Thursday, “the two inflations are not the same”, which is now primarily because of the divergence in fiscal policy between the U.S. and Europe.

President Biden appears to be caught somewhat between a rock and a hard place. Any reduction in government spending in the coming months might help alleviate some of the inflationary pressures but is unlikely to be countenanced with the election looming. If anything, the opposite is much more likely to occur so as to goose activity heading into November. Powell’s option to increase interest rates further to rein in the economy will only serve to exacerbate the deficit, but at the rate we are going they become increasingly justified. The fact that the debate is still primarily around the timing of cuts, and not so much about hikes, seems ludicrous at this current juncture, but again is a function of it being an election year.

There is a large disconnect between equity markets and current interest rates, but this is another area the administration cannot allow to crumble. Proposing to address the excess after the election on the surface always seems like a good plan. Rarely does it play out that way.

Questions/Comments/Concerns

Donal

As I was reminded repeatedly in my previous career, better to be lucky than good.