JHM - April 20, 2024

JHM - April 20, 2024

Despite the fact that the attack Iran launched on Israel last weekend was entirely unprecedented, it was very telegraphed and by design, subsequently ineffective. If I announce to you that I am going to throw a tennis ball your way, and you yourself are Tim Henman well capable of batting back short range missiles, and you can also round up all your friends to stand around and swat away any tennis ball thrown at you, the likelihood of me hitting you in the face with any given ball is extremely low. Hence the lackluster reaction Monday in financial markets and the slide we have seen in oil in recent days. The fact that Iran announced that the attack was aimed to de-escalate I think tells you everything you need to know, despite what the headlines might lead us to believe.

Israel’s response Thursday night was also “aimed to de-escalate”. This is somewhat paradoxical. I’m going to punch you in the face but not that hard so that you don’t feel like punching me back. Irrespective of how it is framed, the overnight recovery in risk-assets again gives the impression that it had achieved this aim in the short-term. All eyes will be back over to Iran now to see if they aim to “de-escalate” things even further.

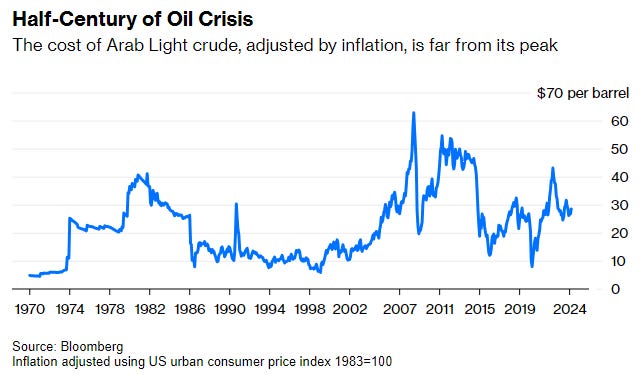

There has been a bit of consternation about the recent rise in the price of oil, largely because of its contribution to President Biden’s angst towards re-election as it is one of the more tangible elements of elevated prices the American consumer can gripe about, but also in part because it impacts future inflation readings. The ongoing restriction of supply from OPEC is helping to ensure prices stay more elevated than they otherwise might be, but once we adjust for inflation, it has gone essentially nowhere for the past twenty years. Tensions in the Middle-East alway adds a premium to the price of oil, motivated by fears over reduced supply following potential conflict or a concurrent blockage in the Strait of Hormuz. Approximately ~20 million barrels per day (bpd) flow through the Strait, just shy of 20% of the world’s daily consumption. As we have discussed here in the past, the oil market is highly inelastic, which means that very small changes in supply can lead to dramatic changes in price in either direction.

The general consensus is that the Saudis and OPEC want oil in the $90-$100 range to ensure they can balance their budgets while at the same time not destroy global demand. A sort of 'Goldilocks' price—not too hot, not too cold. However, when you add to this the inelasticity element, any further escalation of tensions in the middle east that actually does impact supply can have profound consequences. Luckily, all that spare capacity on hand for OPEC producers mean price shocks can in theory be navigated.

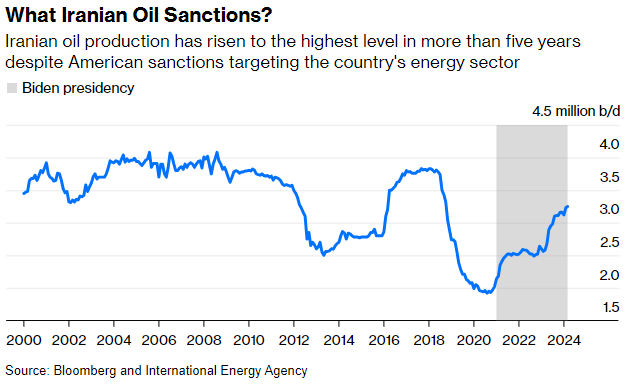

The U.S. sanctioned Venezuela this week for reneging on promises for a fairer election and is in the process of applying more sanctions on Iran. Under the Biden presidency, Iran has managed to steadily increase oil production, despite the numerous sanctions already in place, and currently produces ~3.25 million barrels per day. I would be surprised to see the latest batch heavily impact Iranian production ahead of the election. Should the price start to nudge above $100 per barrel between now and November I think we can expect to see some more supply delivered from the strategic petroleum reserve to massage it back down in time for the vote, just as we saw in the wake of the war in Ukraine.

showing Opec+ has lots of excess crude")

The world is expected to consume ~102 million barrels per day in 2024, and supply is anticipated to be almost exactly equal to this. OPEC has anywhere between 4 million and 6 million in spare capacity. The actual number is up for debate. Take away some of the Iranian production and/or Venezuela (~1m bpd), a partial blockage in the Strait of Hormuz and the market could get extremely tight in a hurry; which goes some way towards explaining the gentle rebuke Biden delivered to Zelensky after Ukraine began targeting some Russian refineries.

The oil sector has had a decent run up in line with the move higher in the commodity, but it remains very much unloved in the investing community. As a share of the market capitalization of the S&P, the energy sector accounts for around 4% while the historical average is at least double that, even as the net income share is closer to 10%.

Exxon Mobil generated $36 billion in Net income in 2023, down from $56 billion in 2022, and has a market cap of $470 billion. Tesla generated net income of $15 billion in 2023, up from $12.5 billion the previous year, and currently has a market cap of roughly the same $495 billion. Exxon paid back a total of $32 billion to shareholders in 2023, $15 billion in dividends and $17 billion in share buybacks. Tesla paid back zero. Yes, I get it, Tesla is a “growth” company, whereas Exxon’s earnings are volatile, can only grow when oil spikes, and the energy sector as a whole had a pretty bad run of things through the 2010s. However, at current prices you could make the argument that Exxon, among other oil companies, is a (relatively) cheap tail risk hedge while also offering inflation protection. Just a thought, which I am sure has played a part in the recent strength.

The market appears very eager to dismiss the Iran/Israel developments, which smacks of complacency. That being said, any non-de-escalatory behavior could lead to chaos no parties involved would want.

Questions/Comments/Concerns

Donal

A healthy debate on the impact of liquidity and the Federal Reserve on financial markets.

Or if you want even more on the oil market