JHM - April 27, 2024

JHM - April 27, 2024

The most important development this week arguably was not the lackluster U.S. GDP release or the accompanying elevated inflation reading, it was what happened in the House of Representatives on Tuesday. Not the aid package for Ukraine specifically, but the granting of authority to President Biden to seize Russian dollar assets and use them to help Ukraine. This has been heavily debated of late, and the ruling is unprecedented in its nature - the speculation now is that it has the potential to have profound implications for U.S. assets going forward, primarily the dollar and Treasury securities.

The ”REPO” provision allows the president to transfer Russian assets to a Ukrainian reconstruction fund. There is currently in the region of $300 billion in Russian foreign exchange reserves frozen by the United States and its allies. The concern permeating now is this step will only serve to further motivate the steady exodus of foreign buyers of U.S. assets. Someone has to buy the Treasuries being issued by the government to fund its’ deficit; if the likes of China, which currently holds in the region of $800 billion worth, are fearful that any sort of hostilities could lead to the rapid confiscation and redeployment of these assets, the incentives for purchasing U.S. assets evaporates. Since the U.S. took the steps to freeze Russian assets in the wake of the Ukraine invasion this concern has been steadily simmering.

showing Chinese funds supercharge gold’s rally")

The step this week is not quite a nail in the coffin, but certainly a(nother) dangerous step towards increased hostilities. Russia reacted by threatening to downgrade its diplomatic relationship in retaliation. The EU has been doggedly avoiding this step up until now, but their hands could very well be forced by the developments this week. President of the European Central Bank, Christine Lagarde, recently remarked the proposal was akin to “breaking the international order that you want to protect.” Of the $300 billion in Russian assets, only about $6 billion appears to be sitting in U.S. banks, with the vast majority held in Germany, Belgium, and France. Unsurprising then that the EU remains reluctant to participate.

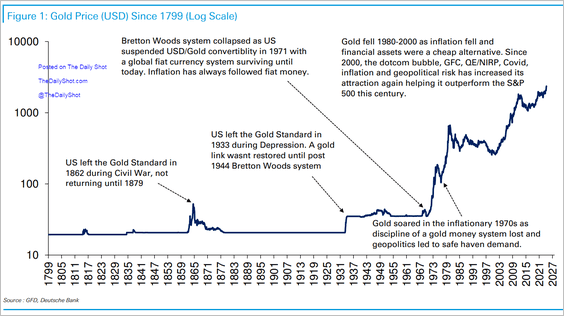

If you want an explanation for the recent surge in gold prices, I think look no further than this week’s development. (We can throw in a dollop of dollar debasement fears and sprinkle in some inflation concerns for good measure to serve up the perfect bullish yellow metal sundae.) Gold is perceived as the ultimate store of value, and physical gold is the type of thing that tin hat wearing conspiracy theorists hide under the floorboards along with cans of tuna and toilet roll. Ultimately, however, if you are a hostile foreign power, hoarding stacks of physical gold bars in your own vaults is certainly one way of avoiding the REPO provision.

Gold has rallied ~15% since the start of the year – not bad for an asset that has averaged an annual return of ~7% over the last decade. This is in the face of higher U.S. yields and dollar, normally headwinds to gold price gains. The People’s Bank of China has been buying gold for 17 straight months, and currently holds 72 million troy ounces, which combined with their Treasury holdings puts their foreign exchange reserves at a value of $3.2 trillion.

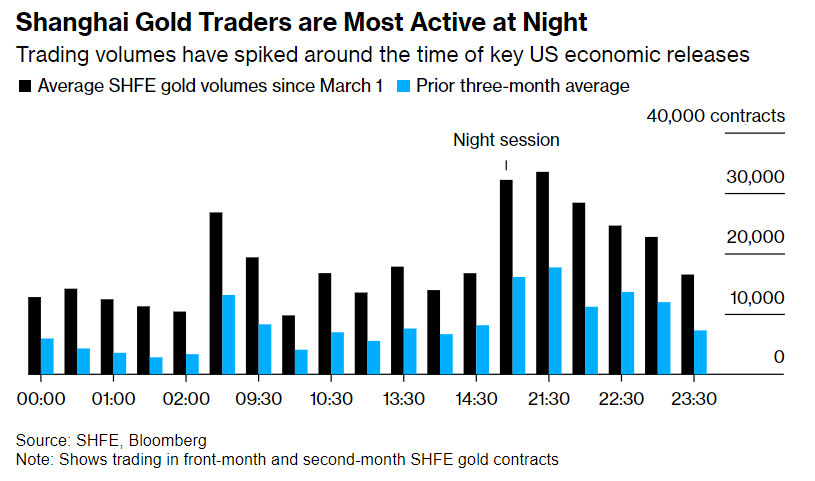

Chinese citizens have increasingly been getting involved of late. This is more likely to speak to their own concerns of currency debasement than fear of their assets being confiscated, but either way it has added more fuel to the oil rally. Trading on the Shanghai Futures exchange perks up right around the time U.S. economic data is released. Higher U.S. inflation readings of late have been widening the spread between U.S. and Chinese interest rates, pushing the USD/CNH exchange rate higher, and fears persist of a much-needed devaluation in that space that could be driving the demand for gold from locals.

showing Chinese gold trading activity explodes")

If China and Russia are not going buy U.S. Treasuries, then who will? The government is already struggling to fund the deficit with interest rates at 5%, and is expected to have to pay something of the order of $1 trillion in interest payments alone over the next year. By persistently running a deficit, it will force increased borrowing just to keep paying off the interest alone. There is a trillion dollars added to the U.S. total debt pile every 100 days at the current rate, which is only accelerating. This is entirely unsustainable. The ways out of this situation are:

Monetize the debt by having the Fed impose yield-curve control and expand the balance sheet to absorb any and all supply of Treasuries the market is unwilling to hold. This will see the complete debasement of the currency and an acceleration of inflation.

Reduce the deficit/aim for a surplus by decreased spending and/or raising taxes – some form of austerity. Neither political party appears to have the word austerity in their vocabulary at present.

Default on the debt – this would be catastrophic for global markets as the U.S. debt is the global reserve asset.

Grow fast enough (with some inflation) such that nominal GDP increases much quicker than the rate at which the debt pile grows, thereby shrinking the Debt/GDP ratio to a more manageable level. Maybe the Artificial Intelligence revolution can spur a productivity boom.. here’s hoping!

If you are a politician which do you vote for? Ideally (4), but failing that, it has to be door number (1)! If you are a central banker with a responsibility to maintain low unemployment and price stability the choice is less clear but likely still ends up at door number (1). In which case you want to own real assets (Gold, Commodities, Energy, Real estate, etc) and not hold paper dollars or U.S. Treasuries as inflation will destroy your purchasing power. I am not convinced this recent bout of elevated inflation persists, especially in light of the weakness in the GDP report, but irrespective of what I think, the market moves in commodity space certainly lends support to the idea that the market has sniffed out that door number (1) is inevitable.

Questions/Comments/Concerns

Donal

Always like including these short little fast ones.