JHM - April 6, 2024

JHM - April 6, 2024

I apologize for the absence of an email last weekend; I understand there is a void in readers’ Saturday without it. Sadly, my attempts to ski did not go entirely to plan, and it ultimately resulted in a trip to the hospital and quite a few stitches in the side of my leg. Thankfully, no serious damage occurred, although it did put an end to any further ventures up the slopes. Probably for the best. Two different doctors laughed in my face when I asked if I could ski the following day. Skiing is hard. Safe to say I need a few lessons.

I mentioned a few weeks back that healthcare could be one of the main beneficiaries of the introduction of artificial intelligence to the industry and there have been some recent developments in the search for a new class of antibiotics that would be the first of its kind in decades. A combined team of individuals from Integrated Biosciences and MIT/Harvard University researchers trained an AI model on 39,000 molecular compounds regarding antibacterial inhibition and toxicity to humans, and then used AI to identify potential candidates out of a database of 12 million compounds commercially available. The search was narrowed down to two from a list of 10,000 potential options that showed strong results. This is akin to asking ChatGPT, “Hey, can you find me a new form of antibiotic, please?” Pretty incredible.

What else has it done? Google’s AI-driven AlphaFold can predict the complex shapes of DNA proteins in a matter of hours at minimal cost, something that would have taken years and huge amounts of money just a couple of years ago.

Infinitely more useful than:

A large element of the job of trading foreign exchange was being able to construct a narrative that would provide an explanation for why something might have happened in markets. The instances where I gave the simple (arguably correct?) explanation for why something went up were that there were more buyers than sellers, which often resulted in a scolding from the person on the receiving end of this nugget of insight. Unsurprisingly also, the “more sellers than buyers” explanation rarely elicited positive responses. The reality at any given moment is that it is virtually impossible to know with 100% certainty what exactly has happened. We can blame comments from Fed officials pertaining to interest rate for why something happened, simply because it is easy and provides us with comfort in the understanding. I could talk about Australian trade data overnight leading to a sell-off, when in reality, there is a corporation in Singapore that has to sell $2 billion to fund an M&A deal. Correct or otherwise becomes almost irrelevant, especially if enough people feel the same way and buy into the proposed narrative.

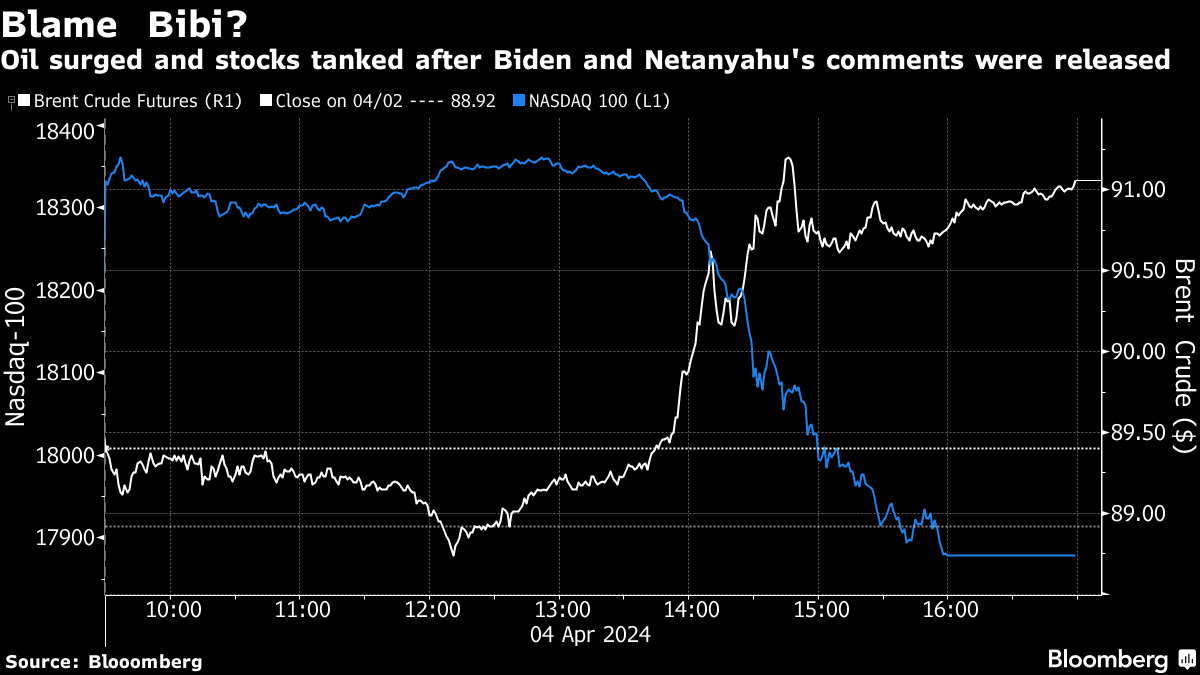

There was a textbook case of this Thursday afternoon as the oil market rallied and stocks took a sharp turn lower following the report of President Biden’s conversation with Israel’s Netanyahu. This was exaggerated further by reports of comments from Fed officials pushing back on the need for rate cuts. The comments from Neel Kashkari were nothing new; he has said the same thing repeatedly and is not able to vote for cuts/hikes either way this year. And the situation in the Middle East is not new. It will remain a source of volatility as and when something happens – this has always been the case!

I am loath to be dismissive of these explanations because, again, it is not what people want. However, I do believe there are times when it really is simply a demand < supply situation. “Profit-taking” is a more formal way of capturing this. The extent to which I was willing to construct a narrative to explain market moves was very much a function of how hungry I was at the time of asking. The hour before lunch was (and will forever be) a period of suboptimal engagement.

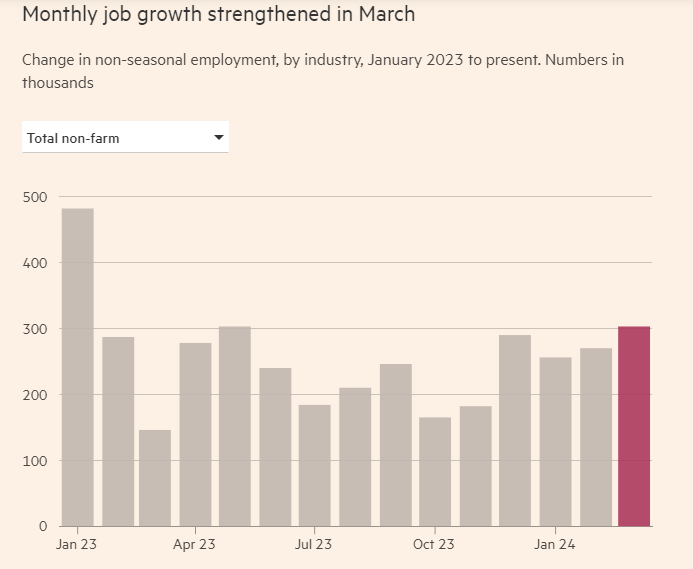

There remains plenty of ongoing speculation as to when the Federal Reserve will cut rates, despite the fact that there is precious little justification at the current juncture. The U.S. economy is flying. The chart above aggregates global economic indicators into a single reading and has the most bullish signal since back in 2021, with the trend very much in the right direction. This was provided further confirmation Friday with yet another robust employment report. What is the problem!

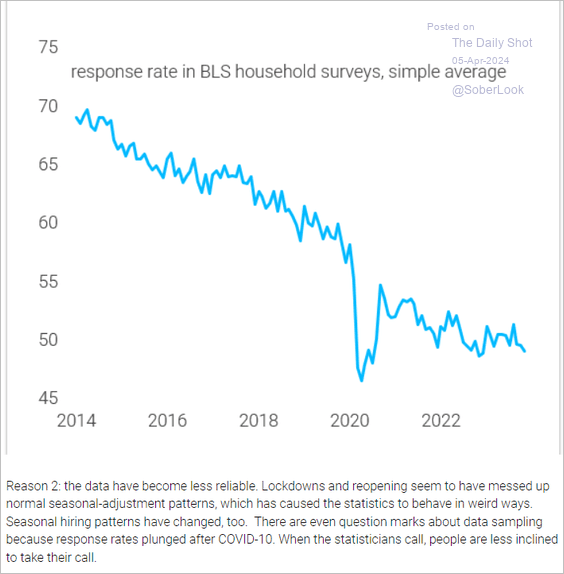

The response rate to the surveys conducted for the monthly employment report has been sitting well below those rates seen prior to the pandemic. Fewer people in the sample means the data becomes more unreliable. And yet judging by the FT plot above, there has been almost no volatility in the survey responses. This is slightly inconsistent, as one would expect the headline employment figure to vary more. Unless it is the case that the participants in the survey just so happen to be all the people increasing employment. Of course this is quite unlikely.

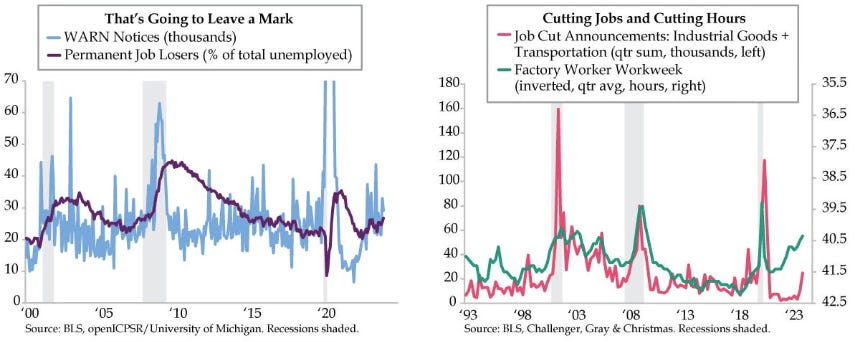

The question then is how to reconcile it with the increased challenger job cut numbers alongside the rising trend of WARN notices and permanent job losers.

Does it matter though? If enough people simply believe the narrative that all is fine in the employment market then the question of what is actually happening below the surface is unlikely to matter. That is until it does.

Questions/Comments/Concerns

Donal

Short little fast one.